MasterCard Authorization Update

Beginning October 14, 2016, MasterCard will introduce new standards for authorization and preauthorization transactions with the singular goal of more efficiently managing the cardholder’s open-to-buy amount on their cards. Currently MasterCard allows for a 15%-20% tolerance between authorization and clearing amounts in many scenarios, non-T&E merchants are unable to process multiple authorizations for a single transaction, and issuers have no way of knowing whether an authorization is a preauthorization, undefined authorization, or final authorization. All three of those are going to change, and the following six rules will explain.

Rule #1—Reverse authorizations within 24 hours of cancellation or finalization of sale with lower amount.

- This will prevent the unused authorization amount from remaining on the cardholder’s account, and free those funds for use.

Rule #2—Merchant must inform cardholder of authorization amount when authorization is an estimated amount.

- Often times cardholders are not informed of the preauthorization amount, and get confused by pending authorizations on their account. It will also aid cardholders in taking necessary steps to avoid negative consequences, such as overdraft fees.

Rule #3— 15% – 20% extra payment guarantee eliminated (except for signature based gratuity).

- Issuers are liable for the extra 15% – 20% extra payment guarantee, even when it is not needed. This can result in the cardholder’s open-to-buy being blocked by an unnecessarily high amount, and prevents them from using those funds.

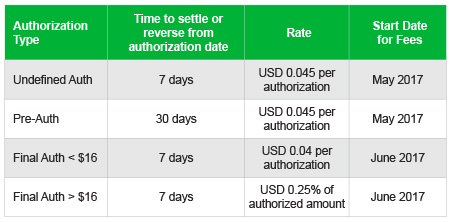

Rule #4—Authorization chargeback protection redefined to 30 days for preauthorizations and seven days for all other authorizations (Does not apply to PayPass or transit aggregated transactions).

- This gives issuers an unambiguous timeline in which they are to hold and release funds, without exposing themselves to chargeback liability.

Rule #5—Authorizations must be clearly identified as either preauthorization, undefined authorization, or final authorization.

- Without the coding of the authorization, issuers are unable to distinguish preauthorizations from all other types of authorizations. So they treat every authorization the same in order to reduce their liability.

Rule #6—Multiple authorizations extended to all merchant types.

- For non-T&E merchants, they must process a separate clearing transaction for every authorization related to a single cardholder event. This will enable those merchants to envelop multiple authorizations into one clearing transaction.

Beginning in May 2017, failure to meet these requirements will result in a processing integrity fee. After these new standards are implemented, a layered approach will be applied to reduce the number of authorizations coded as undefined. By June 2017 less than 50% of authorizations should be coded as undefined. Then, by June 2018 less than 20% should be coded as undefined.